The Stablecoin Regulation Playbook Part 1 — The Global Regulatory Landscape

Written by

Chapter

Share article

Category

Stablecoins are digital currencies designed to maintain a stable value by pegging to an external asset, typically the US dollar. We’ve covered this. We’ve also explored how to build a stablecoin from scratch and how they solve global payroll.

But what about regulation?

Until a few years ago, building a stablecoin meant operating in a regulatory gray zone. There were no widespread guidelines or uniform requirements for issuers and intermediaries. You’d launch, hope you were compliant, and pray you wouldn’t become the following cautionary tale.

Today, the landscape looks significantly different.

Governments and financial institutions have recognized the growing influence of stablecoins on global finance, leading to rapid evolution in how they’re regulated.

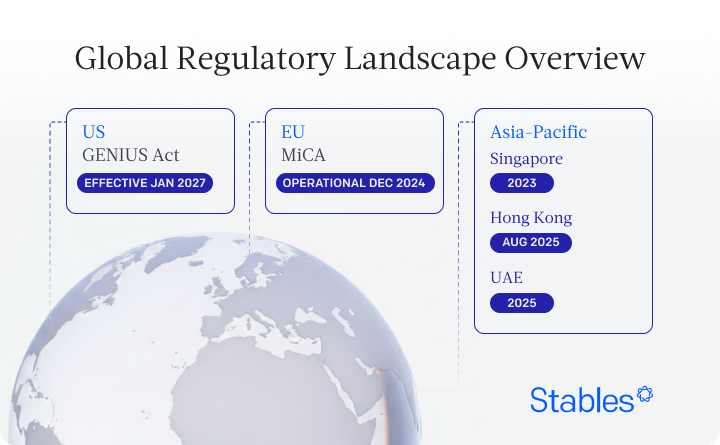

The European Union’s MiCA framework is fully operational. The US passed the GENIUS Act in July. Hong Kong, Singapore, and the UAE have active licensing regimes.

The game has changed. That’s good news. Clear rules open the door to institutional money, banking partnerships, and mainstream adoption. The real challenge now isn’t deciding whether to comply, but understanding these frameworks well enough to design with them in mind from the start.

Consider this your playbook.

The Regulatory Shift

For years, stablecoins existed in a legal gray area. Issuers operated under a patchwork of interpretations, often relying on money transmitter licenses or e-money frameworks that weren’t designed for blockchain-native assets. Enforcement was reactive rather than systematic.

That era is over.

Between 2023 and 2025, major jurisdictions moved from caution to codification. The pattern is consistent: reserve requirements, redemption rights, disclosure obligations, and authorization frameworks. The specifics vary, but the direction is clear.

Europe moved first with MiCA, creating the world’s most comprehensive crypto-asset regulation. The United States followed with the GENIUS Act, establishing federal oversight while preserving state-level paths. Singapore, Hong Kong, and the UAE built their own frameworks, each reflecting local priorities around innovation, stability, and cross-border finance.

The result: stablecoin issuers now have defined paths to legitimacy. The ambiguity that once protected early movers has become a liability for anyone trying to scale.

What the Frameworks Have in Common

Despite jurisdictional differences, a baseline has emerged. Every major framework requires some version of the following:

Reserve backing. One-to-one (or greater) backing with high-quality liquid assets. Reserves must be segregated from operational funds and, in most cases, held with qualified custodians.

Redemption rights. Token holders can redeem at par value, typically within a defined timeframe. Issuers cannot impose unreasonable barriers.

Disclosure and transparency. Regular reporting on outstanding tokens and reserve composition, often with independent attestation or audit requirements.

Authorization. Formal licensing or registration is required before issuing to residents of the jurisdiction.

AML/KYC compliance. Anti-money laundering and know-your-customer requirements are consistent with traditional financial services.

The differences lie in implementation details: what counts as a qualifying reserve asset, how quickly redemption must occur, which regulator oversees authorization, and how cross-border operations are treated.

Why Regulation is Good News

Compliance is expensive and complex. But regulatory clarity unlocks the market you actually want.

Banks, payment processors, and enterprises couldn’t touch stablecoins when rules were unclear. Legal ambiguity meant regulatory risk, and institutions don’t take regulatory risk. Now they can engage, and they’re ready to do it.

What Clarity Enables

Institutional partnerships are now possible. Banks can offer stablecoin services without fear of enforcement. Payment processors can integrate stablecoins into existing rails. VCs and institutional investors can back compliant projects without worrying that regulatory action will destroy their investment. This unlocks larger rounds, strategic investors, and access to institutional-grade infrastructure.

Enterprise adoption accelerates. Companies can use stablecoins for treasury management, payroll, and B2B payments. CFOs and treasurers need regulatory certainty before moving corporate funds into crypto. Now they have it. Compliant stablecoins can integrate with traditional financial systems—bank accounts, payment networks, and trading platforms—creating the distribution and liquidity that enable stablecoins to operate at scale.

The Competitive Advantage

Early movers who nail compliance have a significant head start. Authorization takes a minimum of 6–12 months, infrastructure reserve requires substantial time to build, and regulatory relationships depend on trust earned over the years. Compliance becomes a moat that is hard to replicate quickly, expensive to implement correctly, and requires expertise most teams lack. Get it right early, and you’re defensible in ways pure technology never is.

The Market Opportunity

Stablecoin market cap surpassed $300 billion in October 2025, up from roughly $200 billion at the start of the year. Transaction volume reached $27.6 trillion in 2024, and TRM Labs reports over $4 trillion in volume between January and July 2025 alone. That’s an 83% year-over-year increase.

This is just the beginning. Regulatory clarity accelerates adoption by unlocking institutional use cases that dwarf current crypto-native activity. Citi projects stablecoin issuance could reach $1.9 trillion by 2030 in a base case, or as much as $4 trillion under aggressive adoption.

The founders who win this market won’t be the ones avoiding regulation. They’ll be the ones who understand the frameworks better than anyone else, build compliance into their DNA, and use regulatory clarity as a competitive weapon.

The game has changed. The opportunity just got bigger.

What's Next

This article is the first in a series breaking down stablecoin regulation by jurisdiction. In the coming weeks, we’ll cover:

MiCA: Europe’s Rulebook — authorization, white papers, reserve requirements, and what “significant” status means for issuers targeting EU users.

GENIUS Act: America’s Federal Framework — federal vs. state paths, the $10B threshold, and timelines for compliance.

Asia-Pacific Approaches — Singapore, Hong Kong, and the UAE, including why APAC moved first.

Emerging Frameworks — UK post-Brexit, LATAM developments, and jurisdictions to watch.

Building Compliant Stablecoins — the practical guide to designing for multiple frameworks from day one.

Building Smart in 2025

Stablecoin regulation has matured dramatically. MiCA (EU), the GENIUS Act (US), and Asia-Pacific frameworks now provide clear paths forward. Compliance is complex, but navigable.

At Subvisual, we’ve built stablecoin infrastructure from scratch, including Quill and Orki. We know where technical complexity meets regulatory requirements. If you’re building a stablecoin and want to validate your approach, we can help you create something that’s technically sound, legally defensible, and scalable across jurisdictions.

Building a compliant stablecoin isn’t easy. But it’s worth doing right.