MiCA: Europe’s Rulebook — The Stablecoin Regulation Playbook Part 2

Written by

Chapter

Share article

Category

We’ve covered what the new regulatory landscape looks like and why clarity matters for stablecoin builders. Now it’s time to go deeper.

What does MiCA actually require?

The European Union’s Markets in Crypto-Assets Regulation became fully operational on December 30, 2024. For stablecoin issuers, it means authorization from a national competent authority, a white paper approved before distribution, reserves held in specific configurations, own funds requirements, and redemption procedures that guarantee par value on demand.

The bar is high. Around 45% of issuer applications have been turned down. The transitional periods that let existing operators continue without full compliance are ending—some already have. After July 1, 2026, operating without MiCA authorization means operating illegally across the EU.

But for builders willing to meet the requirements, MiCA offers something new: a defined path to legitimacy in one of the world’s largest markets. Only 16 stablecoins are currently compliant. Banks and institutional partners can work with those issuers without ambiguity.

This article breaks down who needs to comply, what the requirements are, and what the timelines look like.

Token Classification

MiCA covers crypto-assets not currently regulated by existing financial services legislation. It defines three categories: asset-referenced tokens (ARTs), e-money tokens (EMTs), and other crypto-assets.

For stablecoins, classification is simple: if your token pegs to a single fiat currency—like the US dollar or the euro—it’s an EMT. If it’s backed by a basket of assets or multiple currencies, it’s an ART.

Classification matters because requirements differ. Both paths require authorization before issuing to EU residents.

Who Needs to Comply

MiCA applies to two groups:

Issuers: anyone issuing stablecoins to EU residents, regardless of their location.

Crypto-asset service providers (CASPs): exchanges, wallet providers, and custodians offering services in the EU.

If you’re marketing to EU users, you’re in scope, even if your company’s somewhere else. Regulators look at everything: marketing language, messaging aimed at EU residents, domain names, promo plans.

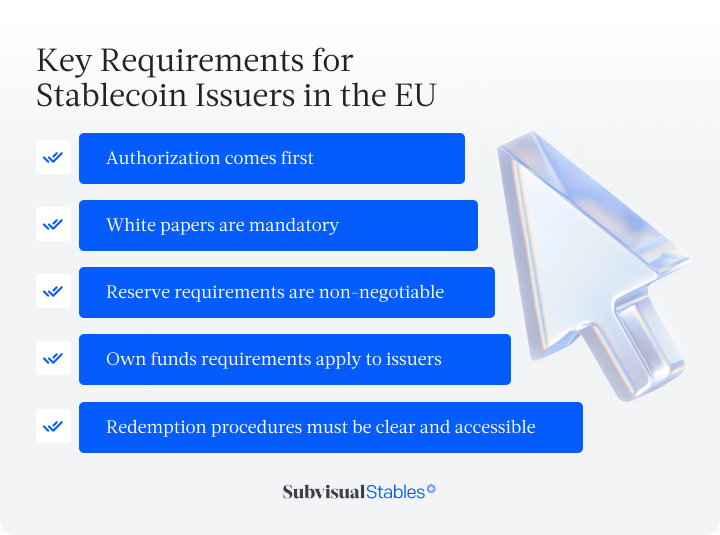

Key Requirements for Stablecoin Issuers in the EU

Authorization comes first. You cannot issue stablecoins in the EU without approval from a national competent authority (NCA). The process varies by member state, with applications accepted since July 2024 for pre-examination, though formal authorization could only be granted after December 30, 2024.

White papers are mandatory. This involves any regulatory disclosure detailing your stabilization mechanism, technology, risks, user rights, and reserve management. Your NCA must approve the white paper before distribution, and material changes require resubmission.

Reserve requirements are non-negotiable. For EMTs, issuers must maintain at least 30% of funds in deposits at credit institutions, with remaining funds invested in secure, low-risk, highly liquid financial instruments. For ARTs, Article 36 requires maintaining a reserve of assets to cover liabilities to token holders, with specific composition and management requirements.

Own funds requirements apply to issuers. Article 35 of MiCA requires asset-referenced token issuers to maintain own funds equal to at least the highest of €350,000, 2% of the average amount of reserve assets, or a quarter of the preceding year’s fixed overheads.

Redemption procedures must be clear and accessible. E-money token holders have the right to redeem at par value at any time.

Ongoing obligations include periodic reporting on outstanding tokens and reserve composition, governance structures ensuring service continuity, internal controls, and consumer protection measures. If your stablecoin becomes “significant”—defined as exceeding 1 million transactions per day or €200 million in transaction value per day within a single currency area—additional requirements apply, including enhanced supervision by the European Banking Authority.

Transitional Measures

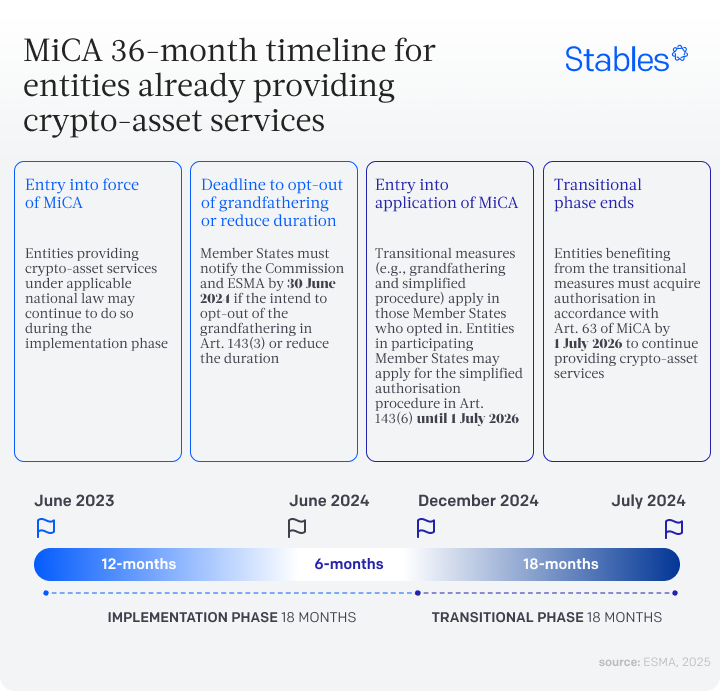

Article 143(3) of MiCA provides a transitional period for entities that were providing crypto services under national law before December 30, 2024. They can continue operating until they’re granted or refused authorization, whichever comes first.

The length of this period varies by jurisdiction. Some member states chose the maximum 18 months, ending July 1, 2026. Others went shorter: 12 months in Germany, Ireland, Greece, Spain, and Liechtenstein (ending December 30, 2025), or just 6 months in Finland, Latvia, Lithuania, Hungary, the Netherlands, Poland, and Slovenia (already ended June 30, 2025).

Once the transitional period ends, all crypto-asset service providers must be fully MiCA-compliant to continue operations. After July 1, 2026, if you don’t have MiCA authorization, it means you’re operating illegally across the EU.

What This Means for Builders

If you’re targeting EU users, MiCA compliance isn’t optional. Authorization requires time, legal fees, compliance infrastructure, and audits.

But compliance also creates what didn’t exist before: legitimacy. Banks and institutional partners can now work with compliant issuers without regulatory ambiguity, which is what stablecoins need to scale beyond crypto-native users.

Start your authorization process early. Budget realistically. If you’re not ready to apply yourself, consider partnering with an already-authorized entity. The regulatory clarity exists. The question is whether you’re positioned to use it.

What's Next

That’s Europe. But what about the United States?

For years, building a stablecoin in America meant navigating overlapping regulators, conflicting guidance, and enforcement actions that didn’t always follow a clear logic. The GENIUS Act changes that. It establishes a federal framework with a dual-path system, defined reserve requirements, and hard deadlines.

Next in the series: the GENIUS Act and America’s federal stablecoin framework—including how it compares to MiCA and what the federal/state choice means for issuers.

Building for Europe

At Subvisual, we’ve built stablecoin infrastructure from scratch, including Quill and Orki. We know where technical complexity meets regulatory requirements. If you’re building a stablecoin and want to validate your approach, we can help you create something that’s technically sound, legally defensible, and scalable across jurisdictions.

Building a compliant stablecoin isn’t easy. But it’s worth doing right.