GENIUS Act: America’s Federal Stablecoin Framework — The Stablecoin Regulation Playbook Part 3

Written by

Chapter

Share article

Category

We’ve covered MiCA. Now let’s cross the Atlantic.

The GENIUS Act was signed into law on July 18, 2025. It’s America’s first federal framework for stablecoins—and it ends years of regulatory uncertainty.

For a long time, building a stablecoin in the US meant navigating a patchwork of state money transmitter licenses, SEC ambiguity, and conflicting agency guidance. You’d pick a path, hope it held up, and watch enforcement actions hit competitors for reasons that weren’t always clear.

That era is closing.

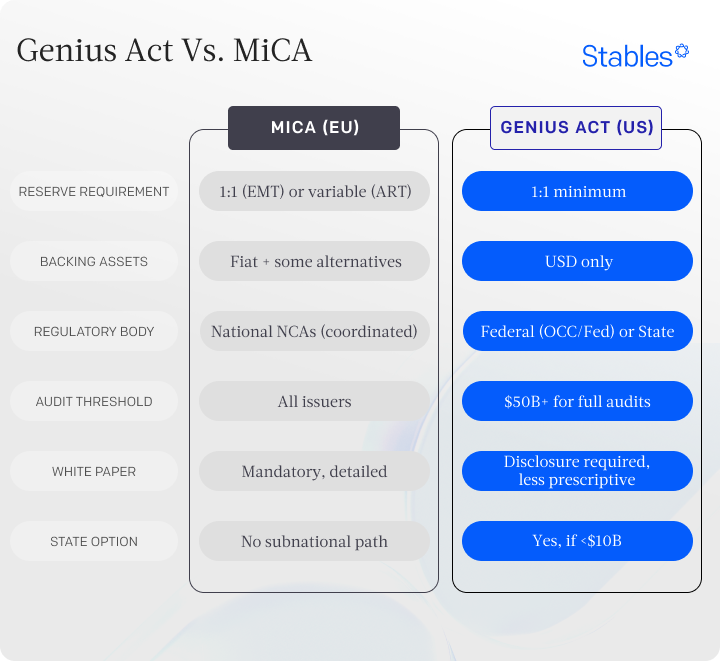

The GENIUS Act establishes a dual-path system: federal oversight through the OCC, or state oversight if your framework is “substantially similar” and you stay under $10 billion. It mandates one-to-one reserves, prohibits rehypothecation, requires monthly disclosure with independent attestation, and applies Bank Secrecy Act compliance across the board.

The timeline is tight. The Act goes live by January 18, 2027—or 120 days after regulators finalize rules, whichever comes first. By July 2028, digital asset service providers can only offer GENIUS-compliant stablecoins.

Banks, payment processors, and institutional players can now integrate stablecoins without legal fog. The rules are defined. The question is whether you’re ready to meet them.

Dual Regulatory Path

You’ve got two options with the GENIUS Act: go federal or state.

Federal issuers get watched by the Office of the Comptroller of the Currency (OCC) if they’re non-banks, or by federal banking regulators if they’re bank subsidiaries.

State issuers can continue with state oversight as long as they have outstanding stablecoins of less than $10 billion and their state’s rules are “substantially similar” to the federal regulations.

The Stablecoin Certification Review Committee (SCRC)—made up of the Treasury Secretary, Federal Reserve Chair, and FDIC Chair—decides if state frameworks are good enough. They all have to agree, which keeps state rules in line with federal standards.

State-issued stablecoins (the government-backed kind) get a pass entirely, which raises questions about how federalism plays out in digital asset regulation.

Key Requirements for Stablecoin Issuers in the US

Issuance is USD-only. You can only issue stablecoins in exchange for US dollars, locking in that one-to-one peg right from the start.

Reserve requirements mean one-to-one backing with high-quality liquid stuff: actual US cash, demand deposits at insured banks, Treasury securities maturing in 93 days or less, overnight repos backed by Treasuries, or registered government money market funds. Reserves must be kept separate, with qualified custodians, and away from your day-to-day operating funds.

Reserves cannot be rehypothecated, meaning you can’t use them to fund other investments. They’re locked exclusively for backing the stablecoins you’ve issued.

Redemption procedures need to be spelled out and easy to find. Par redemption (one-to-one) is a must, and you can’t throw up roadblocks. You’ve got to publish clear policies showing people how to swap their stablecoins back to USD.

Disclosure obligations keep going. You’ll need to put out monthly reports breaking down how many stablecoins are out there and what’s in the reserves—asset types, average maturity, and where they’re held. The composition must be attested by third-party auditors and published monthly.

Audit requirements depend on your size. If you’ve got more than $50 billion in stablecoins floating around, you need audited annual financials from a registered accounting firm. Smaller players get lighter checks, but you still need an independent review.

No interest or yield. Issuers are prohibited from offering interest or yield on issued stablecoins. Your stablecoin is a payment instrument, not an investment product.

Compliance requirements are comprehensive. The Act applies the Bank Secrecy Act requirements to everyone, meaning full AML, sanctions, and KYC rules that apply to financial institutions.

What This Means for Builders

First, you need to decide whether to go federal or state? Going federal means more scrutiny but easier institutional buy-in. State regulation can be faster, but you’ve got to clear the “substantially similar” bar and stay under $10 billion. Cross that line and you’re moving to federal oversight anyway.

You’ll need to budget for compliance infrastructure. Reserve management systems, monthly reporting, independent examinations, and anti-money laundering controls aren’t optional.

Timing counts. If regulators don’t act on your application within 120 days, it’s deemed approved, putting pressure on them to move quickly.

The framework also provides fundamental consumer protections. In the event of bankruptcy, stablecoin holders get a priority claim over other creditors against the issuer’s reserves. This level of protection makes compliant stablecoins more attractive to both institutional and retail users.

International interoperability is baked in. Treasury’s figuring out which foreign regulatory frameworks are “comparable” to the GENIUS Act, potentially allowing foreign-issued stablecoins (like MiCA-compliant ones) to work in the US market through reciprocal deals.

The upside is straightforward: banks, payment processors, and traditional finance can now integrate stablecoins without legal fog. The framework opens up institutional adoption in ways that weren’t possible when stablecoins were in regulatory limbo.

How It Differs from MiCA

The two frameworks push toward a common baseline—full reserves, frequent disclosure, same-day redemption at par—but they diverge in ways that matter for global operations. The GENIUS Act locks reserves into US instruments, such as T-bills and USD fiat. MiCA requires issuers to hold a significant share of reserves onshore in EU accounts for stablecoins marketed inside Europe. The EU sets hard usage caps on non-Euro stablecoins, while the US imposes no currency quotas but restricts foreign issuers through supervisory reach. Licensing paths differ: the OCC and state supervisors control entry in the US, while in Europe, national financial authorities operate under a single passport system backed by the European Central Bank’s veto power for significant tokens. Bottom line: any stablecoin seeking global liquidity must satisfy both frameworks, split collateral across jurisdictions, and run compliance teams capable of meeting two separate disclosure calendars.

What's Next

While Europe and America were debating frameworks, Asia-Pacific was building them.

Singapore finalized its stablecoin framework in 2023. Hong Kong’s Stablecoins Ordinance went live in August 2025. The UAE has multiple regulatory paths across ADGM, DIFC, and VARA. These jurisdictions moved faster, and for builders looking beyond Western markets, they offer distinct advantages.

Next in the series: Singapore, Hong Kong, and the UAE—what their frameworks require, how they differ, and why APAC moved first.

Building for the US Market

At Subvisual, we’ve built stablecoin infrastructure from scratch, including Quill and Orki. We know where technical complexity meets regulatory requirements. If you’re building a stablecoin and want to validate your approach, we can help you create something that’s technically sound, legally defensible, and scalable across jurisdictions.

Building a compliant stablecoin isn’t easy. But it’s worth doing right.