Asia-Pacific: The Early Movers — The Stablecoin Regulation Playbook Part 4

Written by

Chapter

Share article

Category

We’ve covered MiCA and the GENIUS Act. Now it’s time to dive into the market that moved first: Asia-Pacific.

Japan amended its Payment Services Act in 2022, making it one of the first countries in the world with a dedicated stablecoin law. Singapore finalized its framework in August 2023. The UAE’s Central Bank issued its Payment Token Services Regulation in June 2024. Hong Kong’s Stablecoins Ordinance went live on August 1, 2025.

These are fully operational licensing regimes with reserve requirements, redemption rules, AML obligations, and meaningful consequences for non-compliance, not just an experiment.

So, the question isn’t whether APAC takes stablecoin regulation seriously, but why they moved first, and what that means for builders targeting these markets.

Why APAC Moved First

The short answer: different incentives, different urgency.

The US and EU spent years debating how stablecoins fit into existing financial frameworks: whether they were securities, e-money, commodities, or something else entirely. That debate took time, and during that time, stablecoins continued to grow.

APAC jurisdictions faced the same growth curve but reasoned differently. Singapore, Hong Kong, and the UAE are financial hubs that compete globally for capital, talent, and financial infrastructure. Regulatory ambiguity wasn’t a holding pattern, but a competitive risk. If you don’t have clear rules, builders will go elsewhere.

There was also a more structural factor. Singapore and Hong Kong have long-standing traditions of pragmatic, early-stage financial regulation and building frameworks for new asset classes rather than waiting for them to force the issue. The Terra/LUNA collapse in May 2022 accelerated everything. It demonstrated what happens when stablecoins fail at scale, and gave regulators across the region political cover to move quickly.

The result: three distinct frameworks, each reflecting local priorities, that collectively set a global baseline others are now catching up to.

Singapore: The Precision Framework

Singapore’s approach is deliberate by design.

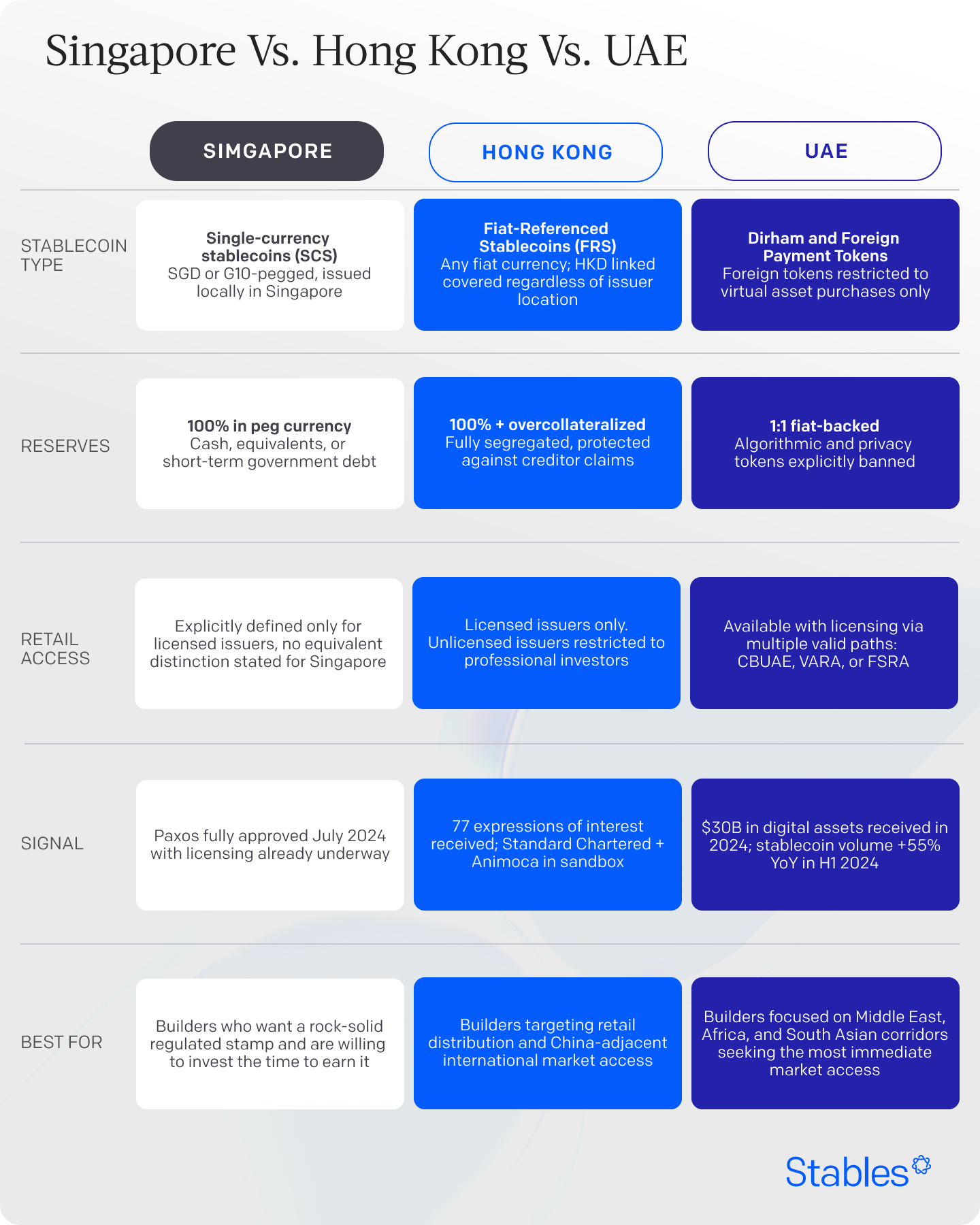

The Monetary Authority of Singapore (MAS) finalized its stablecoin regulatory framework on August 15, 2023, following a public consultation process that began in October 2022. The framework applies specifically to single-currency stablecoins (SCS) issued in Singapore and pegged to the Singapore dollar or a G10 currency.

That scope is intentional. By limiting the “MAS-regulated stablecoin” label to SGD and G10-pegged tokens issued locally, MAS drew a clear line between what it will fully backstop and what remains under general digital payment token rules.

What the framework requires

The label as a signal

The “MAS-regulated stablecoin” designation does more than grant legal permission. It functions as a trust signal in a market where not all stablecoins are created equal. Any person who misrepresents a token as an MAS-regulated stablecoin may be subject to penalties, including financial penalties or imprisonment.

MAS has also limited multijurisdictional issuance for MAS-recognized stablecoins at the initial stage, a deliberate move to establish Singapore as the anchored hub for regulated issuance before allowing cross-border expansion.

The framework is expected to go into full effect in mid-2026. Paxos received full approval from MAS in July 2024, signaling that the licensing process is already underway.

Singapore is also thinking further ahead. Through initiatives like Project Guardian and Project Orchid, MAS is actively testing tokenized asset markets and retail digital currency frameworks, building the infrastructure for stablecoins to integrate into mainstream finance, not just regulate them at the edge.

Hong Kong: The Ambitious New Regime

Hong Kong took a different path and moved faster on implementation.

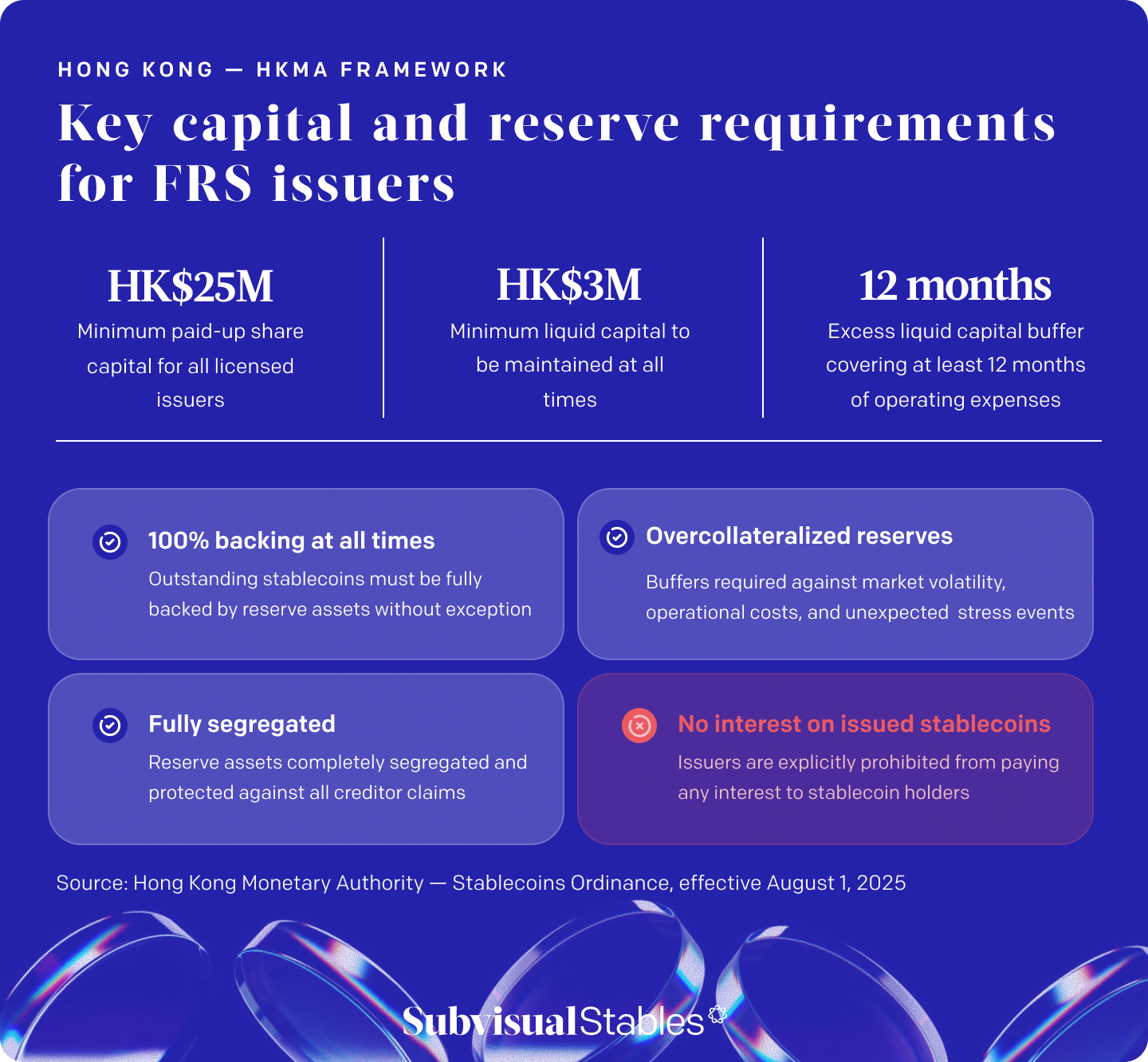

Hong Kong’s Stablecoins Ordinance came into effect on August 1, 2025, making it one of the first jurisdictions globally with a fully operational stablecoin licensing regime. The framework covers Fiat-Referenced Stablecoins (FRS), stablecoins that maintain stable value with reference to one or more fiat currencies, and is administered by the Hong Kong Monetary Authority (HKMA).

A license is required from any FRS issuer operating in Hong Kong, and from any issuer of Hong Kong dollar-linked stablecoins, regardless of where they’re based. Entities that actively market FRS to the Hong Kong public are also required to hold a license.

That extraterritorial reach is significant. If you’re marketing to Hong Kong users, your location doesn’t matter; you’re in scope.

One of the more distinctive features of the Hong Kong regime is that FRS issued by HKMA-licensed issuers can be offered to both retail and professional investors. Stablecoins from unlicensed issuers are restricted to professional investors only. This creates a meaningful advantage for licensed issuers: retail distribution is only available to those who’ve cleared the bar.

Key requirements

Where licensing stands

The HKMA received 77 expressions of interest for stablecoin licenses as of August 31, 2025, but has repeatedly emphasized that only a handful will be granted initially. The first batch is expected in early 2026.

Among early sandbox participants are JINGDONG Coinlink Technology, RD InnoTech, and a coalition of Standard Chartered Bank (Hong Kong), Animoca Brands, and HKT. The coalition’s participation signals something important: traditional financial institutions are treating Hong Kong’s regime as a genuine entry point, not a side experiment.

Hong Kong’s positioning is also geopolitical. Operating within China’s One Country, Two Systems framework, Hong Kong is effectively serving as an international digital assets hub while crypto trading remains banned in mainland China, a regulatory sandbox with global ambitions.

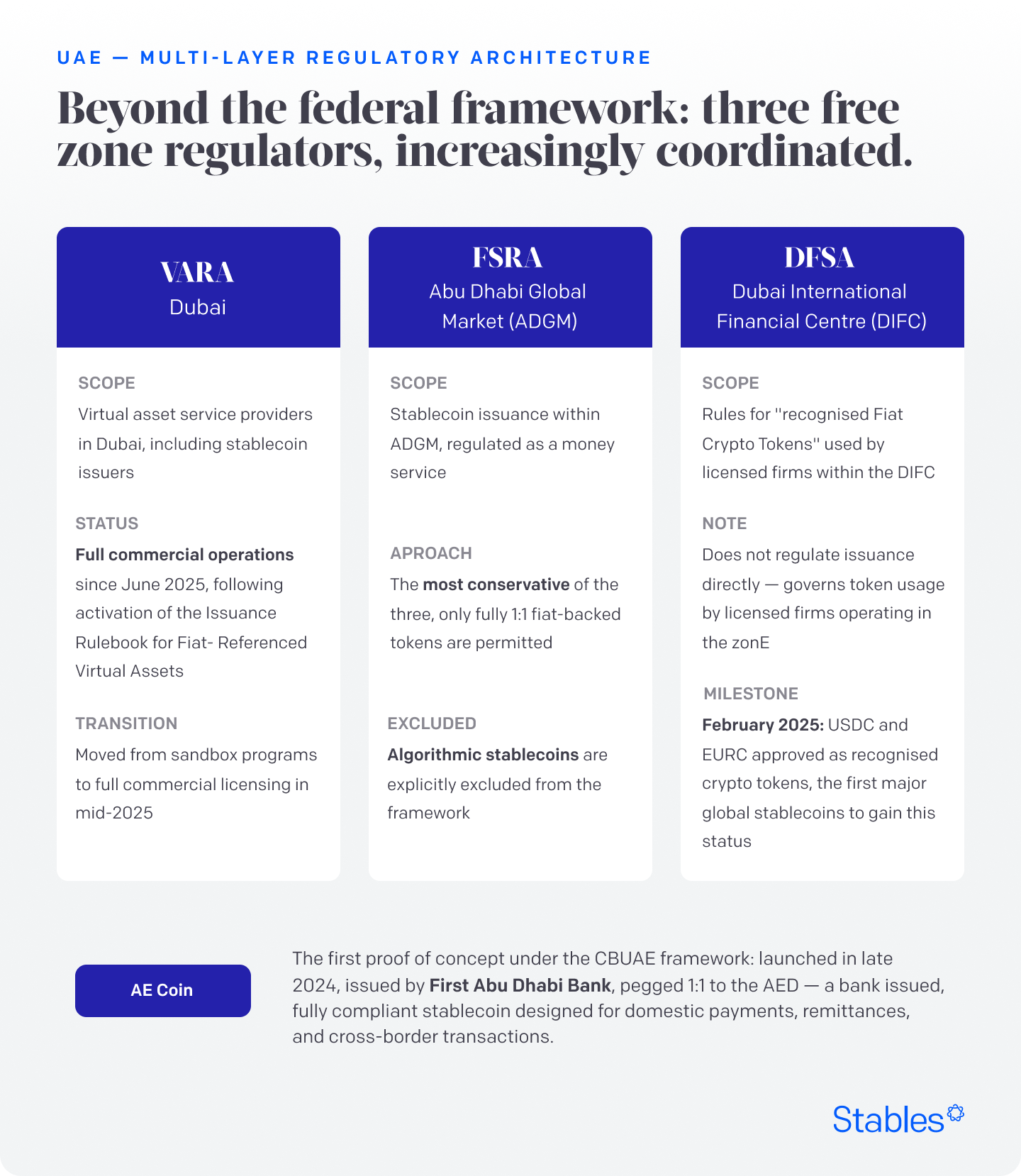

UAE: The Multi-Layer Approach

The UAE doesn’t have one stablecoin regulator. It has several. And they’re increasingly coordinated.

At the federal level, the UAE Central Bank’s Payment Token Services Regulation came into effect in August 2024, establishing a comprehensive framework for stablecoins, referred to throughout as “payment tokens.” A payment token is a virtual asset that maintains a stable value by referencing a fiat currency.

The regulation draws a hard line between two categories: Dirham Payment Tokens, which can be used for any lawful purpose, and Foreign Payment Tokens, which are restricted to the purchase of virtual assets or their derivatives. This distinction is enforceable: after the grace period ended in August 2025, all merchants on the UAE mainland are now required to accept crypto payments only in the form of licensed Dirham Payment Tokens.

Algorithmic stablecoins and privacy tokens are explicitly banned from issuance, promotion, or use as a means of payment in the UAE.

The layered regulatory architecture

Beyond the federal framework, the UAE’s free zones have their own supervisory bodies:

AE Coin: the first licensed dirham stablecoin

AE Coin launched in late 2024 as the UAE’s first fully regulated dirham-backed stablecoin, issued by First Abu Dhabi Bank and pegged 1:1 to the AED. It’s a proof of concept for what the CBUAE framework enables: a bank-issued, fully compliant stablecoin designed for domestic payments, remittances, and cross-border transactions.

The UAE’s broader ambition is explicit: to position the country as the hub for market access to the Middle East, Africa, and South Asia. The UAE received $30 billion in digital assets in the year ending June 2024, and stablecoin volume on UAE exchanges grew 55% year-over-year in H1 2024. The regulation isn’t defensive; it’s infrastructure for an already active market.

How the Three Frameworks Compare

Each jurisdiction reflects different priorities, but the structural baseline is consistent: 100% reserves, licensed issuers, redemption at par, AML compliance. Where they differ is in who can issue, how retail access works, and how much tolerance there is for non-local-currency tokens.

What This Means for Builders

APAC isn’t one market. It’s three distinct licensing regimes, each requiring its own compliance stack, local entity, and regulatory relationships.

The good news: all three are operational. You don’t have to wait for rules to be finalized. The frameworks exist, the licensing processes are running, and the first wave of licensed operators is already being established.

A few practical realities to plan around:

- Local presence matters. Singapore requires that stablecoins be issued locally in the initial stage. Hong Kong expects senior management and key personnel to be based there. The UAE’s CBUAE framework requires local licensing before serving UAE residents. These aren’t administrative formalities. Regulators treat local substance as a proxy for accountability.

- Retail access is a licensing outcome. In Hong Kong specifically, the ability to offer stablecoins to retail investors is only available to licensed issuers. If your business model depends on retail distribution, licensing isn’t optional.

- The “MAS-regulated” label has value beyond Singapore. As institutional and corporate adoption accelerates globally, regulated labels matter for partnerships, banking access, and enterprise integrations. A Singapore framework designation signals something to counterparties in ways that an unlicensed stablecoin can’t.

- Multi-jurisdiction is hard but necessary for global scale. Any stablecoin seeking liquidity across APAC, Europe, and the US has to satisfy MAS, MiCA, and GENIUS simultaneously, split collateral across jurisdictions, and run compliance teams capable of meeting three separate disclosure calendars. That’s not a reason to avoid it. It’s a reason to plan for it from day one.

What's Next

We’ve now covered the major regulatory jurisdictions: Europe, the US, and Asia-Pacific. But there’s a different kind of market we haven’t addressed yet.

Latin America isn’t building frameworks primarily because banks demand them or institutions need clarity. It’s building them because stablecoins are already solving real problems, like dollar access in high-inflation economies, cross-border remittances, and financial inclusion for populations that traditional banking has never reached.

Next in the series: Latin America — Brazil’s DREX, Argentina’s dollarization dynamic, and what it means to build for a market where stablecoins are infrastructure, not innovation.